Discover the role of Blockchain Technology in Electric Utilities for revolutionizing. How can blockchain technology enhance electric grid operations? Explore how blockchain is reshaping the energy sector. Learn about its benefits, real-world use cases, and potential for improving energy grid efficiency.

What Is Block Chain Technology?

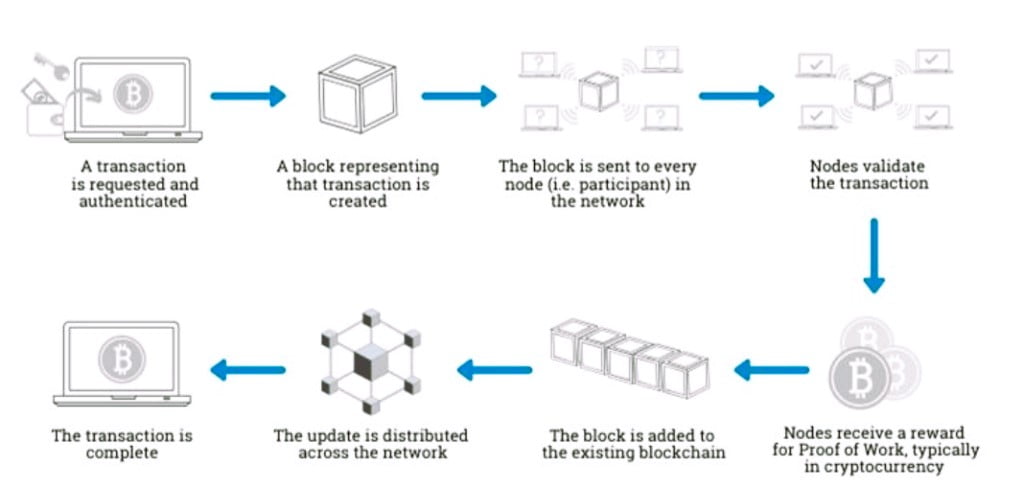

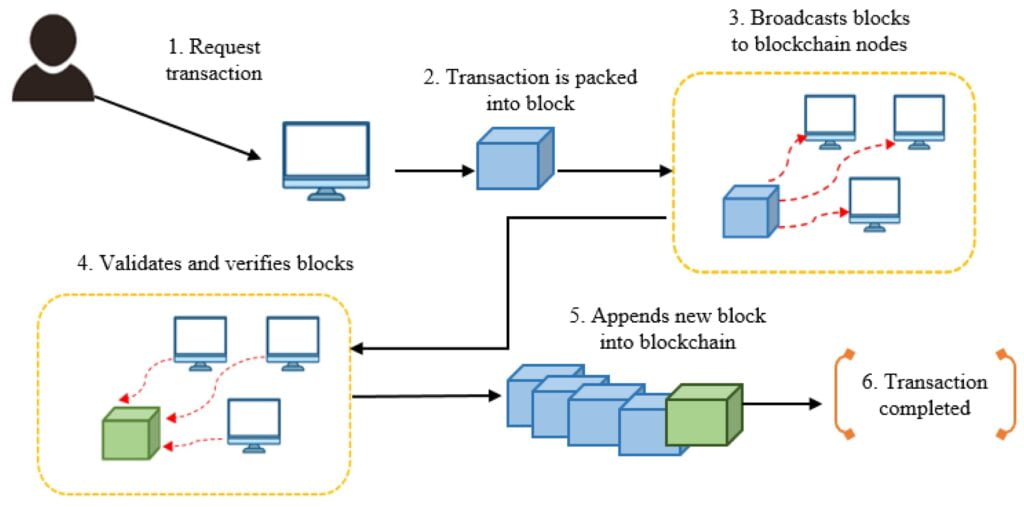

Blockchain is a distributed ledger technology (DLT) that allows for secure, transparent, and tamper-proof recording of transactions. It is a digital database that is shared across a network of computers. Each block in the chain contains a set of transactions, and each new block is linked to the previous block using cryptography. This makes it very difficult to tamper with or alter the data in the blockchain.

Blockchain technology has the potential to revolutionize many industries, including electric utilities. Here are some of the key benefits of blockchain technology:

- Security: Blockchain is a very secure technology because it is tamper-proof. The data in the blockchain is encrypted and distributed across a network of computers, making it very difficult for hackers to access or alter.

- Transparency: Blockchain is a transparent technology because all transactions are recorded on the blockchain and are visible to all participants in the network. This can help to build trust and transparency between parties.

- Efficiency: Blockchain can help to improve efficiency by automating processes and eliminating the need for intermediaries. For example, blockchain can be used to automate the settlement of financial transactions, which can save time and money.

- Immutability: Blockchain is an immutable technology because once data is added to the blockchain, it cannot be changed. This can help to ensure the accuracy and reliability of data.

Read More: Top 10 Cryptocurrencies of 2023

How Blockchain Technology Works?

Blockchain is a distributed ledger technology that uses cryptography to secure its data and ensure its transparency. Here are five basic principles that underlie the technology:

- Distributed Database: Every participant in a blockchain network has access to the entire database, which contains a complete history of all transactions. No single entity controls the data. This decentralization means that each participant can independently verify the transactions of others without needing a middleman.

- Peer-to-Peer Transmission: Instead of relying on a central node for communication, participants in a blockchain network communicate directly with each other. Each participant (or node) stores and shares information with all other nodes, ensuring that data is distributed across the network.

- Transparency with Pseudonymity: Transactions on a blockchain are transparent and visible to anyone who has access to the system. Each participant has a unique alphanumeric address, providing a level of anonymity (pseudonymity). Users can choose to remain anonymous or reveal their identity to others. Transactions take place between these addresses.

- Irreversibility of Records: Once a transaction is recorded in the database and the accounts are updated, the records become unalterable. This is due to the fact that each record is linked to the previous transaction records, forming a chain. The database’s design and algorithms ensure that records are permanent, chronologically ordered, and accessible to all participants.

- Computational Logic: Because blockchain operates in a digital realm, transactions can be tied to computational logic and programmed instructions. This allows users to set up algorithms and rules that automatically trigger transactions between nodes. These programmed “smart contracts” execute actions when predefined conditions are met.

Read More: Solid Waste Management: towards Sustainable Development

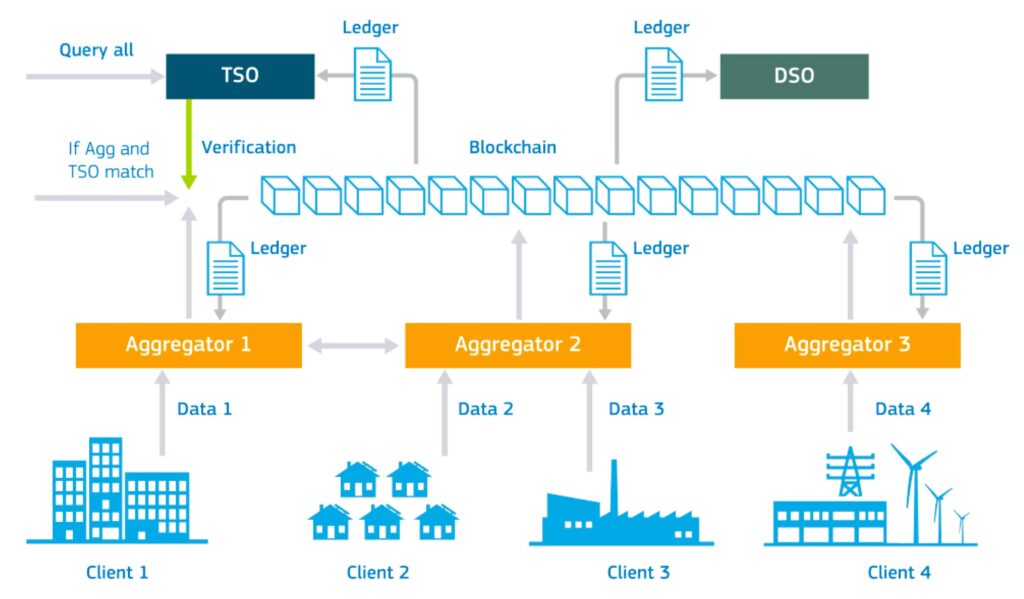

Use Of Blockchain Technology In Electric Utilities

Blockchain technology has the potential to revolutionize the electric utility industry by improving efficiency, transparency, and security. Here are some of the key applications of blockchain Technology in electric utility industry:

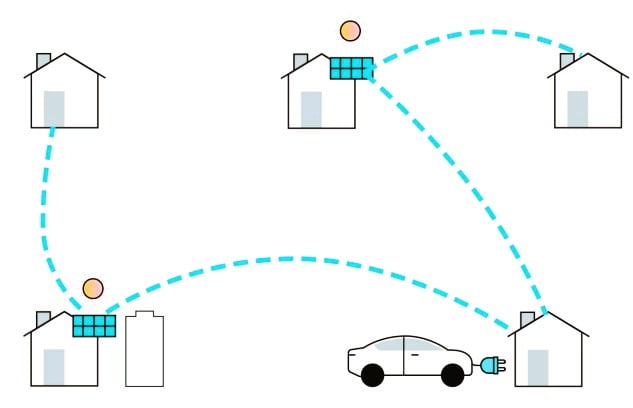

A. Blockchain in Peer-to-Peer Energy Trading

Blockchain can be used to facilitate P2P energy trading, allowing consumers to buy and sell energy directly with each other, without the need for a middleman. This can help to reduce energy costs and improve grid efficiency.

Imagine a neighborhood with several houses equipped with solar panels. These houses generate excess solar energy during the day that they don’t always consume entirely. Traditionally, this surplus energy would be fed back into the central grid, and homeowners might receive compensation from the utility company. However, this process can be inefficient and may not always provide a fair value to the homeowners for their excess energy.

How Blockchain Can Revolutionize Energy Trading

- Decentralized Energy Trading Platform: A blockchain-based platform is created where homeowners can list their excess solar energy for sale. This platform operates on a peer-to-peer (P2P) basis, allowing homeowners to directly trade energy with each other.

- Smart Meters and IoT Devices: Each house is equipped with smart meters and IoT devices that can measure energy production and consumption in real-time. These devices communicate with the blockchain network, recording accurate data about energy generation and usage.

- Smart Contracts for Transactions: Smart contracts are set up on the blockchain. When one homeowner generates excess energy and wants to sell it, a smart contract is initiated. The contract verifies the energy production data and automatically executes the transaction when the conditions are met.

- Transparent and Tamper-Proof Records: Every transaction is recorded on the blockchain, creating an immutable record of energy trades. Homeowners can see the history of transactions, ensuring transparency and trust in the system.

- Secure Payments: Payments for energy transactions are made in digital tokens or cryptocurrencies directly through the blockchain. These transactions are secure, fast, and free from intermediaries.

Real-World Benefits: Blockchain In Peer-to-Peer Energy Trading

- Efficiency: Energy is traded directly between peers, reducing the need for energy to travel back and forth to the central grid. This minimizes transmission losses and increases overall energy efficiency.

- Fair Compensation: Homeowners receive fair compensation for their excess energy, determined by the market demand and supply on the blockchain platform.

- Decentralization: The control over energy trading is decentralized, reducing the reliance on centralized utility companies. This empowers individuals and communities to manage their energy resources.

- Renewable Energy Adoption: Peer-to-peer energy trading encourages the adoption of renewable energy sources like solar, as homeowners have a direct incentive to generate and trade clean energy.

- Resilience: A decentralized energy trading system is more resilient to disruptions and failures. If the central grid experiences issues, the local energy trading can continue to operate.

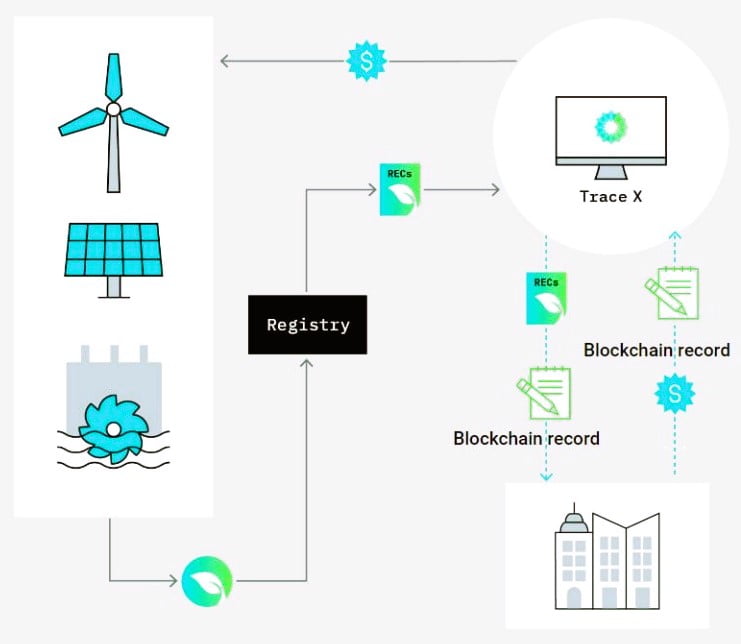

B. Blockchain In Renewable Energy Certificates (RECs)

Renewable Energy Certificates (RECs), also known as Green Certificates or Tradable Renewable Certificates, represent proof that a certain amount of electricity was generated from renewable sources. These certificates are typically used to track and verify the environmental attributes of renewable energy production, allowing organizations to demonstrate their commitment to sustainability.

Blockchain can be used to track and trade RECs, which are certificates that represent the environmental attributes of renewable energy generation. This can help to increase the demand for renewable energy and make it easier for consumers to support clean energy projects.

How Blockchain Technology Can Enhance RECs

- Transparent Record-Keeping: Blockchain technology can provide an immutable and transparent ledger for tracking the generation and ownership of RECs. Each REC’s origin, production, and transactions can be recorded on the blockchain, ensuring the authenticity and integrity of the certificates.

- Creation and Issuance: When a renewable energy generator produces electricity, it is verified by IoT devices or smart meters. This verified production data is then recorded as a new entry on the blockchain, creating a new REC. The blockchain records the exact time, location, and energy source used to generate the electricity.

- Ownership and Trading: Organizations that produce renewable energy can choose to sell their RECs to other entities, like companies looking to offset their carbon emissions. Blockchain enables secure and transparent trading of these certificates. Each REC is represented as a unique token on the blockchain, making ownership transfer straightforward and tamper-proof.

- Traceability and Verification: Through the blockchain, anyone can trace the history of a specific REC, from its creation to its current ownership. This transparency ensures that the certificates are not double-counted or misrepresented, increasing the credibility of renewable energy claims.

- Smart Contracts for Compliance: Smart contracts can be programmed to automatically validate and enforce compliance with regulations and standards. For instance, if a company needs to demonstrate a certain amount of renewable energy use for regulatory purposes, smart contracts can ensure that the necessary number of RECs is held and can trigger notifications if compliance falls short.

Real-World Benefits: Blockchain In Renewable Energy Certificates (RECs)

- Transparency and Trust: Blockchain’s transparency ensures that the origin and ownership of RECs are easily verifiable, reducing the risk of fraud and misrepresentation.

- Efficiency: Automated processes through smart contracts streamline the issuance, trading, and verification of RECs, reducing administrative overhead.

- Market Expansion: The secure and transparent nature of blockchain technology can encourage more organizations to participate in REC trading, expanding the market for renewable energy.

- Regulatory Compliance: Automated compliance enforcement through smart contracts ensures that entities adhere to renewable energy mandates and standards.

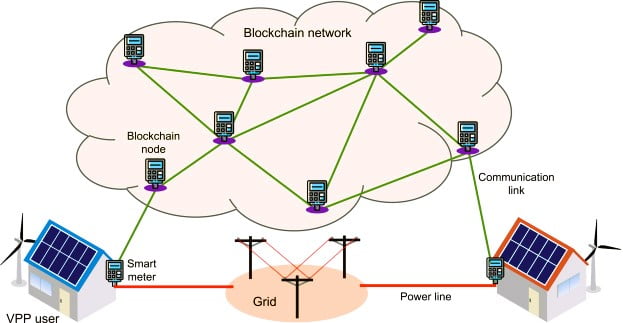

C. Blockchain In Microgrids And Virtual Power Plants (VPPs)

Microgrids are localized energy systems that can operate independently or in conjunction with the main grid. They consist of distributed energy resources (DERs) like solar panels, wind turbines, batteries, and even small generators. Virtual Power Plants (VPPs) are networks of these distributed energy resources that can be remotely controlled and coordinated to operate as a single, integrated power plant.

Blockchain can be used to manage microgrids and virtual power plants, which are small, localized grids that can operate independently of the main grid. This can help to improve grid resilience and flexibility.

How Blockchain Technology Enhances Microgrids And VPPs

- Decentralized Energy Management: Blockchain provides a platform for decentralized management of energy resources within microgrids and VPPs. Each DER has its own IoT-enabled device that communicates with the blockchain network. These devices can monitor energy production, consumption, storage, and demand in real-time.

- Smart Contracts for Energy Transactions: Smart contracts can be programmed on the blockchain to automate energy transactions within the microgrid or VPP. For example, if one household has excess solar energy, it can automatically sell that energy to another household in need, and payments are executed through the blockchain.

- Demand Response and Grid Stabilization: Blockchain-enabled microgrids and VPPs can participate in demand response programs. When the main grid faces high demand or instability, the blockchain can trigger certain DERs to adjust their energy output to support grid stability. Participants are rewarded for their contribution.

- Provenance and Auditing: Blockchain records the entire lifecycle of energy transactions, from production to consumption. This provides transparency and traceability for auditing purposes, ensuring that energy is generated and consumed as claimed.

Real-World Example: Blockchain In Microgrid In Rural Community

Imagine a rural community with limited access to the main power grid. The community sets up a microgrid that combines solar panels, wind turbines, and batteries. The microgrid is connected through blockchain technology.

- Energy Production and Distribution: Each household with solar panels or wind turbines generates its own energy. The energy production data is recorded on the blockchain, indicating how much energy is available in the microgrid.

- Peer-to-Peer Energy Trading: A blockchain-based platform allows households to buy and sell energy directly. If one household produces more energy than it needs, it can sell the excess to neighboring households via smart contracts. Payments are made in digital tokens or cryptocurrencies through the blockchain.

- Grid Stability and Demand Response: When there’s a sudden spike in energy demand or grid instability, the blockchain triggers specific households with excess energy to provide additional power, helping stabilize the microgrid and contributing to the overall energy balance.

- Transparency and Auditing: The blockchain ensures that energy transactions are transparent and tamper-proof. Residents can verify the origin of the energy they’re buying, enhancing trust in the system.

D. Blockchain In Smart Meters

Smart meters are advanced energy meters that record electricity consumption in real-time and can communicate this data to both consumers and utility companies. They provide valuable insights into energy usage patterns and enable more efficient energy management.

Blockchain can be used to store and manage data from smart meters, which can help to improve grid efficiency and customer engagement.

How Blockchain Technology Enhances Smart Meters

- Secure Data Sharing: Smart meters generate a continuous stream of energy consumption data. This data can be stored securely on a blockchain, providing a tamper-resistant and transparent ledger of energy usage.

- User Control and Privacy: Blockchain technology allows users to maintain control over their energy data. Consumers can grant specific permissions for data access, ensuring their privacy is respected while enabling authorized parties (like utilities or energy service providers) to access necessary information.

- Decentralized Energy Trading: If a user generates excess energy through solar panels, the blockchain can facilitate peer-to-peer energy trading. Smart contracts on the blockchain automatically execute transactions when the user’s excess energy is sold to neighbors or the grid.

- Billing and Payments: Blockchain enables automatic and accurate billing based on real-time consumption data from smart meters. Payments can be made through the blockchain, ensuring transparency and reducing disputes.

Real-World Example: Blockchain In Smart Meters

Consider a neighborhood where each household has a smart meter connected to the blockchain:

- Solar Energy Generation: Households with solar panels generate excess energy during sunny periods. Their smart meters record this surplus production.

- Smart Contracts and Peer-to-Peer Trading: Using blockchain, these households can enter into smart contracts that automatically sell their excess energy to neighbors when demand is high or during cloudy periods. Payments are automatically settled through the blockchain.

- Transparent Energy Transactions: All energy transactions, including energy sales, purchases, and payments, are recorded on the blockchain. Each participant can verify the energy source and transactions in real-time, ensuring transparency.

E. Blockchain In Automatic Settlement Of Energy Trades

Energy markets involve the buying and selling of electricity and other energy resources between producers, consumers, and traders. The settlement of these trades often involves complex and time-consuming processes, including reconciling various parties’ records, verifying transactions, and processing payments.

Blockchain can be used to automate the settlement of energy trades, which can help to reduce costs and improve efficiency.

How Blockchain Technology Enhances Energy Trade Settlement

- Transparent Transaction Records: Blockchain creates a shared and immutable ledger that records every energy trade transaction. This ledger is accessible to all participants, ensuring transparency and eliminating the need for reconciling discrepancies between different parties’ records.

- Smart Contracts for Automation: Smart contracts are programmed on the blockchain to automatically execute predefined actions when certain conditions are met. In the context of energy trade settlement, smart contracts can automate the entire process, triggering payments and updating ownership records when energy trades are confirmed.

- Real-Time Verification: Energy trade data, such as trade agreements and settlement details, are recorded on the blockchain in real-time. All participants have access to this verified information, reducing the need for manual verification and reducing settlement delays.

- Decentralized Settlement: Unlike traditional settlement systems that rely on centralized intermediaries, blockchain enables peer-to-peer settlement. Parties involved in the trade interact directly through smart contracts, eliminating the need for intermediaries and reducing settlement costs.

Real-World Example: Blockchain In Electricity Wholesale Market

Imagine an electricity wholesale market where utility companies, renewable energy producers, and consumers participate. They use a blockchain platform for trade settlement:

- Trade Agreement: A utility company agrees to purchase excess solar energy from a renewable energy producer at a certain price per kilowatt-hour (kWh). They define the terms of the trade agreement, including volume and price.

- Smart Contract Creation: The trade agreement details are coded into a smart contract on the blockchain. The smart contract includes conditions for trade execution, payment, and settlement.

- Trade Execution: As the renewable energy producer generates and supplies electricity to the utility company, the smart meter records the energy delivered. This data is automatically fed into the blockchain.

- Automatic Settlement: Once the predetermined conditions are met (e.g., energy delivery confirmed), the smart contract automatically triggers the settlement. Payment is made in digital tokens directly through the blockchain to the renewable energy producer’s account.

F. Blockchain In Fraud Prevention In Energy Industry

Fraud in the energy industry can involve various activities, such as meter tampering, billing manipulation, and unauthorized access to energy resources. Traditional methods of detecting and preventing fraud can be time-consuming, costly, and often reactive.

Blockchain can be used to prevent fraud in the energy industry, such as electricity theft and meter tampering.

How Blockchain Technology Enhances Fraud Prevention In Energy Industry

- Immutable and Transparent Records: Blockchain creates a tamper-resistant and transparent record of all energy-related transactions. This includes energy production, distribution, consumption, and payments. Any attempt to manipulate or alter data is immediately detectable, reducing the likelihood of fraud.

- Decentralized Verification: Blockchain’s decentralized nature means that data is verified by multiple participants in the network. This consensus mechanism ensures that fraudulent activities, such as unauthorized changes to energy meter readings, are unlikely to go unnoticed.

- Smart Contracts for Automated Checks: Smart contracts can be programmed to automatically trigger predefined checks and verifications. For example, if a sudden spike in energy consumption is detected beyond a certain threshold, the smart contract can initiate an alert for further investigation.

- Real-Time Data Monitoring: IoT devices and sensors collect real-time data from various points in the energy system. This data is directly recorded on the blockchain, allowing for constant monitoring and immediate detection of anomalies.

Real-World Example: Blockchain In Meter Tampering Detection

Consider a scenario in which a homeowner attempts to manipulate their energy meter to report lower energy consumption:

- Blockchain-Connected Smart Meter: The homeowner’s smart meter records energy consumption in real-time and stores this data on the blockchain.

- Verification Nodes: Multiple verification nodes on the blockchain network cross-reference the energy consumption data from the smart meter with historical consumption patterns and data from neighboring meters.

- Anomaly Detection: If the smart contract detects a significant deviation from expected energy consumption patterns, it triggers an alert. This could indicate potential meter tampering or unauthorized access.

- Immediate Investigation: The energy provider receives the alert and launches an immediate investigation. Since the tampering attempt is detected in real-time, corrective measures can be taken promptly to prevent further fraud.

Future Prospects Of Blockchain In Electric Utilities

The future holds exciting possibilities for blockchain in the energy sector. From enabling microgrids to fostering renewable energy integration, blockchain can accelerate the transition to a sustainable energy future. However, challenges like scalability and regulatory hurdles need to be addressed.

FAQs For Blockchain Technology In Electric Utilities

Why Blockchain Technology is Used?

Blockchain technology is used to create secure, transparent, and decentralized systems for recording transactions and managing data. It aims to eliminate the need for intermediaries, enhance trust, reduce fraud, and streamline various processes across industries.

What is an Example of Blockchain Technology?

An example of blockchain technology is the Bitcoin blockchain, which is used to record and verify transactions of the cryptocurrency Bitcoin. Another example is Ethereum, a blockchain platform supporting various applications beyond just digital currency.

What is Blockchain in Simple Terms?

Blockchain is a digital ledger that securely records and stores transactions across multiple computers. It operates in a decentralized and transparent manner, providing a tamper-proof and traceable record of events.

What is Blockchain used for Today?

Blockchain is used for various purposes today, including cryptocurrency transactions, supply chain management, digital identity verification, smart contracts, healthcare data management, and more.

Is it Difficult to Learn Blockchain?

Learning blockchain can vary in difficulty depending on your background and the depth of understanding you seek. It requires a grasp of cryptographic concepts, distributed systems, and programming skills, but there are resources available to make the learning process smoother.

What is the another Name of Blockchain technology?

Another name for blockchain technology is “Distributed Ledger Technology” (DLT).

Where is Blockchain stored?

Blockchain data is stored on each participating node in the network. Each node has a copy of the entire blockchain, ensuring redundancy and resilience.

Can a Blockchain be Hacked?

While blockchain is highly secure due to its cryptographic nature and decentralized structure, no system is completely immune to attacks. However, the design of most blockchains makes hacking extremely difficult and costly.

Who is the CEO of Blockchain?

There is no single CEO of blockchain technology itself, as it’s a concept and technology rather than a company. However, various companies in the blockchain space have their own CEOs.

Who invented Blockchain?

Blockchain was conceptualized by an individual or group using the pseudonym Satoshi Nakamoto, who also created Bitcoin, the first cryptocurrency utilizing blockchain technology.

What are 3 uses of Blockchain Technology?

Three uses of blockchain technology are cryptocurrency transactions, supply chain management, and digital identity verification.

Which language is used in Blockchain?

Different programming languages can be used to develop blockchain applications, including languages like Solidity (for Ethereum smart contracts), JavaScript, Python, Go, and more.

Who are the key players in Blockchain?

Key players in the blockchain space include Ethereum, Ripple, Binance, ConsenSys, IBM, and various government and financial institutions working on blockchain projects

Which is better AI or Blockchain?

AI (Artificial Intelligence) and blockchain serve different purposes. AI focuses on creating intelligent systems, while blockchain focuses on decentralized and secure record-keeping. Both technologies can complement each other in certain applications.

Who owns a Blockchain?

Blockchains are decentralized networks, so they are not owned by a single entity. Participants collectively maintain and validate the blockchain, removing the need for a central owner.

What are the 4 different Types of Blockchain Technology?

The four main types of blockchain technology are Public Blockchains, Private Blockchains, Consortium Blockchains, and Hybrid Blockchains.

How to Invest in Blockchain?

You can invest in blockchain technology by purchasing cryptocurrencies like Bitcoin or Ethereum, investing in companies working on blockchain projects, or exploring blockchain-related investment funds.

Does Amazon use Blockchain?

Yes, Amazon Web Services (AWS) offers various blockchain-related services and tools for organizations to develop and deploy blockchain applications.

What are the most used Blockchain Types?

The most commonly used types of blockchains are Public, Private, and Consortium blockchains. Public blockchains are open to anyone, private blockchains are restricted to specific entities, and consortium blockchains are maintained by a group of organizations.

Is Bitcoin an Example of Blockchain?

Yes, Bitcoin is one of the most well-known examples of blockchain technology. It uses blockchain to record and verify transactions of the cryptocurrency.

Who hosts Blockchain Data?

Blockchain data is hosted and maintained by the network of participating nodes in a decentralized manner. Each node holds a copy of the entire blockchain data.

Who records the Blockchain?

The blockchain is recorded and maintained by the distributed network of nodes. Each node verifies and records transactions, creating a consensus on the state of the blockchain.

What Is Crypto Wallets and Their Types?

Discover the world of crypto wallets. Keep your digital assets safe! Learn about hardware, software, paper, online, and mobile wallets…

Tesla Stock Price Prediction 2023, 2025, 2030, 2040, 2050, 2060

Are you thinking about buying Tesla shares? Do you want to figure out if it’s a good investment? If so,…

Apple Stock Price Prediction 2023, 2025, 2030, 2040, 2050, 2060

Are you thinking about buying Apple shares? Do you want to figure out if it’s a good investment? If so,…

How Global Warming Leads To Climate Change?

Explore the undeniable connection between human activities, greenhouse gas emissions, and the far-reaching impacts on our planet’s climate. Find insights…

How To Buy Bitcoin (BTC) In 2023?

Learn how to buy Bitcoin (BTC) with ease. This comprehensive guide covers step-by-step instructions, FAQs, and expert insights to help…

How Neural Networks And Deep Learning Works?

“Curious about neural networks and deep learning? Dive into the world of deep learning with an in-depth exploration of neural…

3 thoughts on “Blockchain Technology In Electric Utilities”